The actual rate of return to the bank's structural wealth management products high-yield into a "painting cake"?

Dongfang Net reporter Cheng Qi reported on February 23: In recent years, bank wealth management products have become the new favorite of consumer financial management. However, in the bank's wealth management products, some structured wealth management products that began to be released by banks have become synonymous with “the most unreliable†wealth management products. This morning, the Shanghai Consumer Protection Committee announced that it can be bought for Shanghai consumers. The evaluation results of 627 bank structured wealth management products, the expected probability of yield is unknown, the degree of realization is low; the investment management process is opaque; the disclosure of public information is not the main problem of structured wealth management products.

Older people believe that investment risk is lower

It is understood that the sample of this study is the result of the evaluation released by the Shanghai Consumer Protection Committee and the Shanghai Normal University Business School after a year of industry interviews and expert arguments, including 17 banks 2016. 627 products that expired in the first half of the year, and 8 types of targets.

The results show that about 35% of the product banks are rated as the lowest risk level, and nearly 60% are the lower risk level, which is consistent with the consumer's impression. More than half of the information is disclosed once or twice. The 13 products had the highest level of consumer protection, rated as five stars, accounting for 2.07%, and 251 were rated as four stars, accounting for 40.03%.

According to a survey of consumption expenditures of 2011 elderly people by the Shanghai Consumer Protection Committee in 2016, about 11.3% of the elderly have purchased wealth management products, of which 22.8% of the elderly will purchase structured wealth management products recommended by the bank. About 76.9% of the elderly who purchase institutionalized wealth management products believe that the risk of structured wealth management products is low.

High-yield into a "painting cake" is just "looking beautiful"

But is this really the case? According to the results of this study, the “expected rate of return†is a term that is easily misunderstood by consumers.

Yang Baohua, an associate professor at Shanghai Normal University's School of Business, said that during the research process, the “expected rate of return†only looked beautiful, and then in the actual purchase process, there was a large range of expected yields, complex revenue structure, and unknown probability of realization. In other cases, investors tend to ignore many of these factors, and go straight to the highest rate of return, the results are often expected to fall through.

For example, the shares of OCBC Bank are added to the 17th stock-linked products in 2015. The expected maximum yield is 18%, the expected minimum yield is 0, and the actual rate of return is zero. Jiangsu Bank “Jubao Wealth Exclusive No. 4 (Structural) 1609â€, the expected minimum rate of return is 1.5%, the expected maximum rate of return is 18.5%, the actual rate of return is only 1.5%... The expected rate of return is greater than 6%. Of the eight products, the actual yields of the six models tend to be the lowest.

What is even more confusing for investors is that in the case provided by the Consumer Protection Committee, Jiangsu Bank’s “Jubao Wealth Exclusive No. 4 (Structural) 1512†product has a complicated structure and a “knock-out clauseâ€. Once the increase exceeds 16%, consumers can only get a 3% annualized rate of return; if there is a two-way fluctuation, the rate of return is even more difficult for consumers to understand.

Yang Baohua said that the actual expected rate of return on the simulation of the product is mostly concentrated at the level of 2%, and the probability of achieving a higher rate of return is relatively small.

Actual rate of return, information disclosure, "hiding cat"

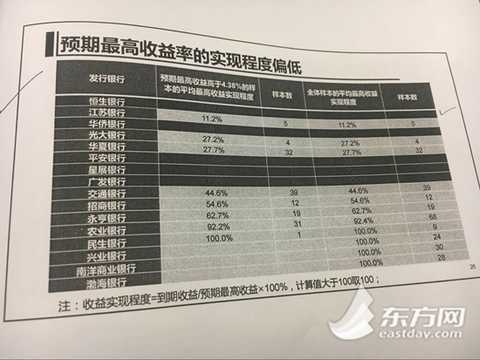

In addition, the Consumer Protection Committee also announced a list of banks with a low expected rate of achievement. Among them, Hang Seng, Jiangsu, Overseas Chinese, China Everbright, Huaxia and other banks are in the forefront, although the highest expected return is higher than 4.38%, then The degree of implementation is not satisfactory.

For example, Hang Seng Bank's implementation level is only 6.3%, Jiangsu Bank is 11.2%, OCBC Bank is 13.3%, and the average maximum income is below 30%, that is, if consumers are told that the rate of return is 10%, But in the end only 0.63%, 1.12%, 1.33%;

Yang Baohua believes that the investment management process of such products is opaque, including not publishing counterparty information, sources of derivative investment funds are not clear, and product cost information disclosure is not sufficient. In the disclosure of public information, the product specification lacks uniform specifications, and the information availability is not strong, which is not convenient for investors to compare.

Consumer Protection Committee: Bank design less play technology and more conscience

In this regard, Dean of the Shangshang University Business School, Yan Xuncheng, said that whether banks can become the dominant players in the effectiveness of financial markets depends on whether the information is symmetrical and whether the transactions are fair and transparent, but many banks are lucky and want to make more profits. Therefore, "active asymmetry".

Yan Xuncheng believes that the bank's products can not harm consumers, to ensure that consumers have the lowest returns, not only the expected range, but no probability. The more effective the market is, the longer-term bank's long-term gains are, and banks should look to the long-term. He suggested that banks should conduct stress tests when designing products and make information as fair as possible.

Tang Jiansheng, deputy secretary-general of the Shanghai Consumer Protection Committee, also said that banks should also play less technology when designing products, pay more conscience and be responsible to consumers.

Structural wealth management products

Structured wealth management products refer to a new type of financial products formed by combining fixed-income products such as deposits and zero-coupon bonds with financial derivatives (such as forwards, options, swaps, etc.). The rate of return on structured wealth management products usually depends on the performance of the linked assets. According to the attributes of the linked assets, structured wealth management products can be roughly subdivided into foreign exchange hooks, index hooks, stock hooks and commodity hooks.

Structural wealth management products were born in the early 1980s. In the 1990s, they exploded in the European and American markets, becoming the most innovative type of financial wealth management products in the past 20 years. In 2002, domestic structured products began to appear in the form of structured deposits. In September 2005, the China Banking Regulatory Commission issued the Interim Measures for the Administration of Personal Banking Business of Commercial Banks, which incorporated structured deposits (especially derivatives) into the integrated wealth management business.

Financial management

Industry insiders to buy structured wealth management products

1. Familiar with the hook target

Investors should try to choose the products they are familiar with in the market before purchasing the linked wealth management products. Investors should have a certain judgment on the trend of the linked variety, combined with the income calculation method of the bank wealth management products, whether the probability of the product obtaining the expected high return is large, and then making investment decisions.

From a solid point of view, the probability of a structured wealth management product linked to interest rates reaching the expected maximum rate of return is high, and the probability that a structured wealth management product linked to a stock achieves the expected maximum rate of return is low, and investors should choose carefully.

2. See the proportion of the insurance

At present, structural wealth management products are mostly in the form of capital preservation, but we must not think that the capital preservation is 100% guarantee of the security of the principal. We must carefully read the proportion of the capital preservation in the product manual. Some products are partially guaranteed products. If the ratio of capital preservation is 90%, it means There is a possibility of a loss of 10% of the principal.

It is worth noting that there are also structured wealth management products that are non-principal-guaranteed floating income categories. This means that even if the principal is totally depleted, it is possible. Therefore, the type of income and the proportion of capital preservation must be clearly seen when purchasing structured wealth management products.

3. Do a diversified investment

The probability that a structured wealth management product achieves the expected maximum rate of return is relatively low, and it is also possible to lose the principal. Therefore, when purchasing, investors should preferably use part of the investment funds to invest and diversify the risk.

In addition, investors also need to choose different forms of income-based hooks based on their own risk appetite.

(Editor: HN666)

Men'S Casual Leather Shoes,Men'S Casual Shoes,Casual Shoes,Comfortable Men Casual Shoes

Guangdong XDDD Footwear Crop. Ltd , https://www.xdshoe.com