Guomao Futures: PTA long and short intertwined shocks

Hot spot funds flow to thousands of stocks to evaluate stocks to diagnose the latest rating simulation transaction

Client

Registration : The annual banking festival “2017 China Banking Development Forum and the 5th Bank Comprehensive Selection Awards Ceremony†hosted by Sina Finance will be held on August 24th at the Westin Beijing Financial Street Hotel, so stay tuned . [registration entry]

This month, the PTA market showed a sharp rise and then quickly fell back, with a monthly increase of 6.92%. In the first half of July, PTA benefited from the large-scale maintenance of domestic equipment, low operating rate and continuous destocking, while downstream demand showed the opposite situation. The high demand for superimposed construction led to mismatch between supply and demand, so PTA prices went up all the way. The premium was quickly labeled as a monthly discount, and then the market confirmed on the evening of July 10 that the constant force of 2.2 million tons/year due to equipment failure, the maintenance period was extended to mid-August, and the news again detonated the market's sentiment, PTA once shocked The daily limit and the large amount of funds have contributed to a big upswing. In the second half of the month, Hankang Petrochemical's 1.1 million tons/year line and Jialong Petrochemical's 600,000 tons/year unit restarted, and the PTA start-up load increased. After the downstream PTA surged, the price of grey cloth increased less than raw materials, and the profit margin of the weaving production chain was Compression, tight capital led to poor price transmission, polyester factory production and sales decline and accumulation phenomenon, and the terminal part of the weaving factory due to high temperature weather production and shutdown, the operating rate dropped from 74% to the current 59%, double The pressure on the side caused the PTA high to fall sharply.

Looking at the next month, the optimistic expectation of crude oil is there, supporting the PTA to a certain extent. On the installation side, with the restart of Hengli Petrochemical's 2.2 million tons/year plant and the 65,000-ton/year installation of Yizheng Chemical Fiber Co., Ltd. and the 1.5 million tons/year installation maintenance plan of Honggang Petrochemical, the construction will be maintained at around 69%. If the downstream polyester plant maintains a relatively high start, the PTA market supply will remain tight, but considering that the current low-end weaving of the terminal will cause a certain drag on the PTA, and the processing fee will have further downward space. In view of the short-term PTA, it is difficult to make a big difference. In August, the probability of the PTA1709 contract fluctuated mainly between 5050-5400. The PTA1801 contract considered the factors of shifting the position and changing the month and the market liquidity is still tight. Compared with the PTA1709 contract, the contract may be more strengthened, and the anti-set may be of concern. On the unilateral point of view, the 1709 contract is not suitable for re-opening the speculative month of the delivery month. 1801 can try to do more for the light warehouse, for reference, strictly control the risk!

First, the market review

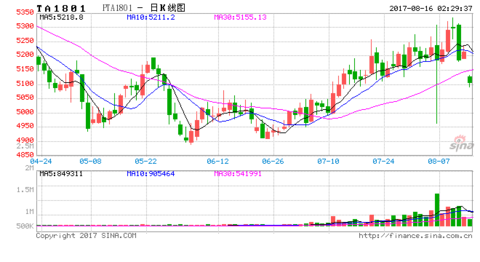

Chart 1: PTA1709K line graph

Source: Guomao Futures, Wenhua Finance

This month, the PTA market showed a sharp rise and then quickly fell back, with a monthly increase of 6.92%. In the first half of July, PTA benefited from the large-scale maintenance of domestic equipment, low operating rate and continuous destocking, while downstream demand showed the opposite situation. The high demand for superimposed construction led to mismatch between supply and demand, so PTA prices went up all the way. The premium was quickly labeled as a monthly discount, and then the market confirmed on the evening of July 10 that the constant force of 2.2 million tons/year due to equipment failure, the maintenance period was extended to mid-August, and the news again detonated the market's sentiment, PTA once shocked The daily limit and the large amount of funds have contributed to a big upswing. In the second half of the month, Hankang Petrochemical's 1.1 million tons/year line and Jialong Petrochemical's 600,000 tons/year unit restarted, and the PTA start-up load increased. After the downstream PTA surged, the price of grey cloth increased less than raw materials, and the profit margin of the weaving production chain was Compression, tight capital led to poor price transmission, polyester factory production and sales decline and accumulation phenomenon, and the terminal part of the weaving factory due to high temperature weather production and shutdown, the operating rate dropped from 74% to the current 59%, double The pressure on the side caused the PTA high to fall sharply.

Second, the industry chain analysis

2.1 International crude oil

As of the close of July 28, the US New York Mercantile Exchange WTI crude oil index futures contract price closed at 49.96 US dollars / barrel, a monthly increase of 6.37%. At the same time, the London ICE European Futures Exchange Brent crude oil futures contract price closed at 52.54 yuan / barrel, a monthly increase of 6.14%.

Chart 2: B-line chart of Brent crude oil index contract (unit: USD/barrel)

Chart 3: K-line chart of US crude oil index contract (unit: USD/barrel)

Source: Guomao Futures, Wenhua Finance

This month, crude oil rose sharply, and the market continued to send good news. First, the growth rate of Baker Hughes oil drilling slowed down. According to the latest data, the number of oil drilling in the US increased by 2 in the week ending July 28, increasing for the third consecutive week to 766, and a total of 10 in July, the lowest monthly increase since May last year. Second, the decline in crude oil inventories is good for continued fermentation. The EIA crude oil inventory data was declining throughout July, and as the US entered the summer oil peak period, the sharp decline in gasoline inventories also provided momentum for the oil market to rise. Finally, Nigeria's limited production further boosts oil prices. The world's major oil producers met in St. Petersburg, Russia on the 24th. Saudi Arabia said it will reduce crude oil exports to 6.6 million barrels per day in August, down 1 million barrels per day from the same period last year, and OPEC reached a non-OPEC oil producer. The agreement limits Nigerian crude oil production and encourages other oil-producing countries to comply with production cuts. The above-mentioned positives support the oil price to rise further.

However, there are still several risks in the oil market. First of all, the Russian meeting did not show any real positives. It was only the optimistic expectations of oil-producing countries, including improved demand in the second half of 2017, restrictions on exports and strict implementation of production cuts. Saudi Arabia lowered August production and export pressures. Second, US crude oil production. Although there has been a decline, the output of 48 states is still increasing. It is normal for Alaska's summer production to decline. After the fall, the total US crude oil production still has room to rise. Finally, crude oil inventories have dropped significantly, of which exports have increased substantially. The increase in construction is the main reason, and gasoline inventories are still small. Looking at next month, risks exist, especially geopolitical risks, but oil prices are still expected to rise under the influence of this month.

2.2PX spot

Chart 4: PX price and profit margin (unit: USD/ton)

Source: Guomao Futures, wind

This month, the Asian PX showed a volatility upward trend. The average monthly price of CFR China this month was US$794.8/ton, up 0.61% from the previous month; the average monthly price of FOB Korea was US$775.8/ton, up 0.76% from the previous month.

At the beginning of the month, due to the sharp increase in production in Libya and Nigeria, the international oil price remained weak and the domestic PX demand level was weak. The tired inventory situation continued and the negotiation was slightly lower. In the middle of the month, due to the increase in Chinese demand, the supply pressure was temporarily eased, and the crude oil data was favorable. The international oil price remained at a high level, the PX cost end was well supported, and the current PTA price was due to the smooth progress of destocking, so the upstream and downstream dual-use PX negotiations rose; at the end of the month, the international oil price was high, the cost side momentum was strong, and the Asian PX market bought The interest in the disk surged and boosted. The news of the Italian conference reduced production and the US crude oil production and inventory fell. PX negotiations rose sharply. However, the downstream PTA was adjusted back due to high processing fees and polyester plant production and sales pressure. Under the dual effect, the price increase of PX at the end of the month narrowed.

2.3 PTA market

Chart 5: PTA internal and external disk spot prices

Source: Guomao Futures, Wind

In July, the PTA market showed a sharp rise and then quickly fell back. In the first half of the month, PTA benefited from the large maintenance of domestic equipment, low operating rate and continuous destocking, while downstream demand showed the opposite situation. The high demand for superimposed construction led to mismatch between supply and demand, so PTA prices went up all the way, and the water rose rapidly from the distant moon. In the evening of July 10, the market confirmed that Hengli 2.2 million tons / year due to equipment failure, the maintenance period was extended to mid-August, the news once again detonated the market's long-term sentiment, PTA once hit the daily limit, The massive increase in funds has contributed to a big upswing. In the second half of the month, Hankang Petrochemical's 1.1 million tons/year line and Jialong Petrochemical's 600,000 tons/year unit restarted, and the PTA start-up load increased. After the downstream PTA surged, the price of grey cloth increased less than raw materials, and the profit margin of the weaving production chain was Compression, tight capital led to poor price conduction, polyester factory production and sales decline and accumulation phenomenon, and the terminal part of the weaving factory due to high temperature weather production and shutdown, the operating rate dropped from 74% to the current 59%, double The pressure on the side caused the PTA high to fall sharply.

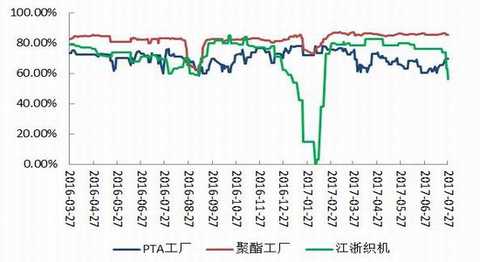

Figure 6: PTA industry chain start load rate

Source: Guomao Futures, Wind

This month's PTA operating rate showed a decline and then slowly rebounded, while the polyester plant has been at a high starting point. The Jiangsu and Zhejiang looms fell sharply at the end of the month, from a high of 74% to 56%. At present, Hengli Petrochemical's 2.2 million tons/year installation will be shut down for maintenance on June 23, and it is scheduled to restart in early August; Yizheng Chemical Fiber 650,000 tons/year plant plan will be shut down for 15-20 days on August 6 and Honggang Petrochemical will be 1.5 million tons/ The annual equipment maintenance plan may be advanced to August, and it is expected that PTA will start around 69%-73% next month.

Figure 7: PTA processing interval (unit: yuan / ton)

Source: Guomao Futures, Wind

This month, the PTA spot market price surged sharply, while the cost-side PX price increase was relatively limited, and the processing interval was basically completely affected by the PTA price. The highest processing interval quickly rushed to a high of 1,200 yuan / ton in recent years, and then quickly declined. The current spot processing range is still around the high of 840 yuan / ton, the futures processing range is around 879 yuan / ton, the short-term continues to fall Possible.

2.4 Polyester market

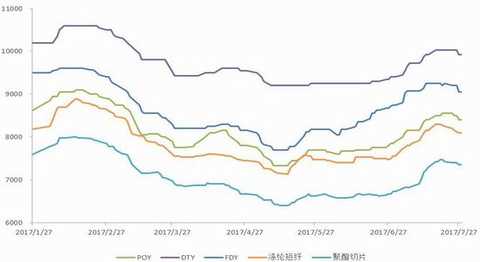

Chart 8: Polyester price trend (unit: yuan / ton)

Source: Guomao Futures, Wind

The price of polyester products this month has fallen sharply with the price of raw material PTA, and it has also shown a trend of falling back. This year, regular products such as polyester taffeta and silk have continued to sell well, prompting the speed of returning funds from weaving factories to be faster than in previous years, and the enthusiasm for raw material procurement has been significantly improved. At the same time, the environmental protection rectification of water jet looms in Jiaxing, Keqiao and Wujiang areas, the industry expects the supply of grey cloths to further decline, prompting some cloth manufacturers to place orders in advance to lock the price, resulting in the early release of some peak seasons in the second half of the year, the price of polyester products is large On the rise, some companies have experienced the phenomenon of default.

However, as the price of polyester products rises too fast, the price increase of grey cloth is far less than the increase of raw materials. The profit margin of weaving production is greatly reduced. In addition, the number of new orders has decreased compared with the previous period. A few factories have experienced production reduction and parking. Currently, weaving machines in Jiangsu and Zhejiang provinces The operating rate dropped sharply. Mainly because of the fact that many terminal factories are mainly based on inventory production, the consumption of funds by high raw materials and high stocks has increased, and the repayment of funds in some areas has been tight. Second, during the period from mid-July to early August, it is the main period of high temperature power in the Jianghuai and Jiangnan areas. It lasts for ten consecutive days. Due to the health and safety of the factory workers, weaving Factories will also consider downtime or appropriate production cuts. Subsequently, the production, sales and heat of polyester products declined, and the price also dropped slightly.

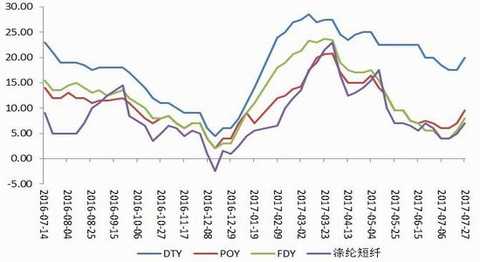

Figure 9: Statistics on polyester inventory days (unit: day)

Source: Guomao Futures, Wind

This month, the entire polyester industry inventory experienced a significant decline and then slowly recovered at the end of the month. At present, the average stock of polyester staple fiber is around 7 days, the average POY of polyester filament is around 9.5 days, the average FDY of polyester filament is around 8 days, and the average of polyester filament DTY is around 20 days. In the next month, affected by high temperature weather and peak-avoidance, it will continue to have a negative impact on the operating rate of the loom. The rigid demand in the market will lead to an increase in the sales pressure of the polyester factory. It is expected that the polyester inventories will continue to rise slowly.

Third, operational recommendations

Looking at the next month, the optimistic expectation of crude oil is there, supporting the PTA to a certain extent. On the installation side, with the restart of Hengli Petrochemical's 2.2 million tons/year plant and the 65,000-ton/year installation of Yizheng Chemical Fiber Co., Ltd. and the 1.5 million tons/year installation maintenance plan of Honggang Petrochemical, the construction will be maintained at around 69%. If the downstream polyester plant maintains a relatively high start, the PTA market supply will remain tight, but considering that the current low-end weaving of the terminal will cause a certain drag on the PTA, and the processing fee will have further downward space. In view of the short-term PTA, it is difficult to make a big difference.

In August, the probability of the PTA1709 contract fluctuated mainly between 5050-5400. The PTA1801 contract considered the factors of shifting the position and changing the month and the market liquidity is still tight. Compared with the PTA1709 contract, the contract may be more strengthened, and the anti-set may be of concern. On the unilateral point of view, the 1709 contract is not suitable for re-opening the speculative month of the delivery month. 1801 can try to do more for the light warehouse, for reference, strictly control the risk!

Strictly control the position, stop profit and stop loss.

Guomao Futures Sun Yuhuan

Sina statement: Sina's posting of this article for the purpose of transmitting more information does not mean agreeing with its views or confirming its description. Article content is for reference only and does not constitute investment advice. Investors operate on this basis at their own risk.Enter [Sina Finance and Economics Unit] Discussion

Thermal Socks Series,Thermal Socks,Heat Holders Socks,Insulated Socks

JINGJIANG SHIJIA INTERNATIONAL TRADING CO.,LTD , https://www.jjsjinternational.com